Social Security full retirement age and benefits

Social Security full retirement age and benefits. According to a Transamerica Center study, 24% of U.S workers count on Social Security as their main source of income during retirement. As you start planning for retirement it is important to learn about the benefits you can expect from Social Security.

Social Security benefits: some basics

You must be at least 62 to receive social security benefits. If you choose to receive the benefits before you reach your full retirement age, your benefits may be reduced. Depending on your age, the benefit may be reduced by as much as 30%.

You can also choose to delay receiving benefits from Social Security until you are 70. If you delay taking the benefits, the amount of your benefit will increase.

An early retirement can reduce benefits. In contrast, a delayed retirement can increase benefits. The timing of your retirement will depend on your personal situation. Before making a decision on when to start receiving benefits from Social Security, you may want to consider the following scenarios.

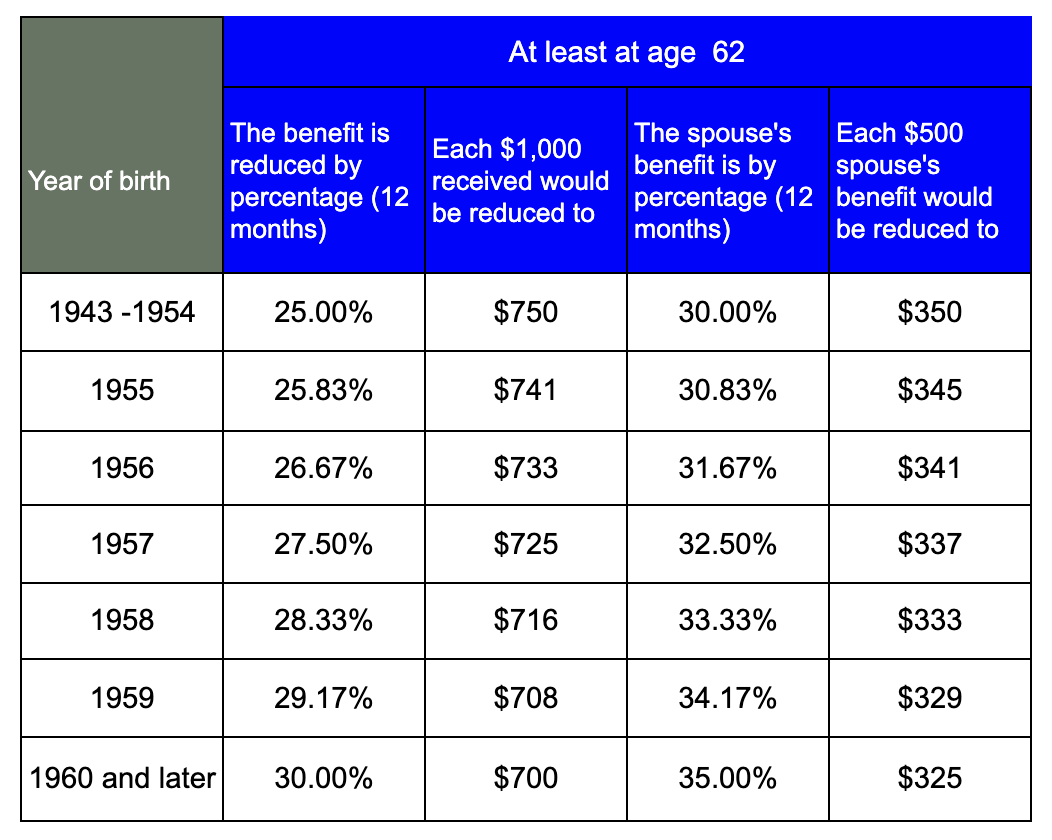

Social Security early retirement

You can start to receive Social Security benefits when you reach 62 years old. However, if you choose to receive the benefits before you reach your full retirement age, the benefits may be reduced by as much as 30% depending on your date of birth.

For reference, you can see the percentage reduction of benefits for a specific date of birth from the chart below.

(all percentages are rounded)

For instance, you were born in 1955 and received your Social Security benefits at the age of 62. Your benefit might be reduced by 25.83% or each $1,000 that you received would be reduced to $741. In addition, your spouse benefit on your Social Security record would be reduced by 30.83%. Or each $500 that your spouse received would be reduced to $345.

Social Security full retirement age

Americans are living longer. Therefore, the Congress passed the law to increase the retirement age beginning with the year of birth 1938 and later. The retirement age is increased by several months for every birth year until it reaches 67 for people born 1960 and later.

You can receive the full retirement benefit amount when you reach full retirement age. Otherwise, your benefit will be reduced by some percentage if you choose to receive the benefit before you reach your full retirement age.

For reference, you can see your full retirement age from the chart below from the Social Security.

(All percentages are rounded)

If your birthday was on the 1st of the month, your benefits or full retirement benefits will be referred to as if your birthday was on the previous month. For instance, you were born on January 1st. Then, your birth year will be counted as the previous year for Social Security benefits. In addition, you must be at least 62 years old to start receiving the benefits.

Social Security benefits for spouses

If you do not have enough Social Security credits to qualify for your own retirement benefit, and your spouse has enough credits, you could apply for benefits through your spouse.

If you do qualify for the benefits on your spouse’s Social Security record, the maximum benefits that you can receive is 50% of your spouse’s full retirement benefits.

To qualify for the spouse benefits, you must be at least 62 years old or at any age if you care for a child that is under the age of 16 or disabled. The child also qualifies to receive benefits based on your spouse’s Social Security records.

Full retirement age calculation

The retirement benefit that you and your spouse would receive increases from the age of 62 up to the full retirement age. Your retirement benefit may be different depending on your age and year of birth.

For reference, you can use the links below to check your benefits and the full retirement age based on your year of birth: 1943 -1954, 1955, 1956, 1957, 1958,1959,1960 and later.

Social Security benefits calculator

Your Social Security benefits will vary based on many factors such as your birthday, cost of living adjustment, and applicable U.S laws and policies.

How much Social Security benefit will you get?

You will not know the actual amount of your Social Security benefits that you will be given until you apply for it. However you can always check out an estimated amount by using the Social Security Quick Calculator, the Retirement Estimator, or the Estimate Retirements Benefits calculator. You can use these estimates to plan for your future retirement benefits at different ages.

Delayed Retirement Credits

If you delay your benefits after your full retirement age, your benefit increases with delayed retirement credits. The annual delayed retirement credit varies from 3% – 8% by year of birth. The delayed retirement credits will stop increasing when you reach 70 years of age.

The chart below, shows the annual increase in benefits due to delayed credits, based on year of birth.

For instance, you were born in the year between 1941-1942, your annual retirement credits were 7.5% of your retirement benefits.

Planning for your Social Security benefits

Your monthly Social Security benefits depend on your age and when you start to receive benefits.

If you choose to receive the benefits before you reach your full retirement age, you will receive the benefits for a longer period. However, your benefit will be reduced by a certain amount depending on your year of birth. On the contrary, if you choose to receive the benefit at your full retirement age or later, your benefits will be larger; but you will receive it for a shorter period of time.

Moreover, before you decide to receive your Social Security benefits, you may want to consider the following conditions. The conditions may make impacts on your benefits.

Working while receiving Social Security benefits

If you are working while receiving your Social Security benefits. Plus, you are between the age of 62 and your full retirement age, there are limitations on your benefits. However, when you reach your full retirement age, your earnings do not affect your benefits. After you reach full retirement age, your benefit amount will be recalculated. As a result, you will receive credits for any months that you did not receive benefits due to your earnings.

Your life expectancy

According to the Social Security Administration, the Social Security benefit began making monthly payments in 1940. From 1940 to 2020, the life expectancy of men has increased by 6 years to 84. Similarly, women’s life expectancy has increased by 7 years to 86.5.

Everyone should make their own plan on when to retire. No one can know exactly how many years they will spend in their retirement. You may expect to have a long life if your family has a history of longevity. However, you may live long even otherwise. It is wise to have a plan to support yourself in your golden years. Depending on your individual scenario, you may choose to start receiving benefits earlier or at the full retirement age.

Having other sources of income

If you have other income sources to support your living and do not need your benefits right away, you may want to delay receiving your benefits. Some people may receive early retirement from their employer. In such cases, some pensions that include a Social Security equivalent supplement will stop automatically at the age of 62. The supplement stops because they assume you will apply for your retirement benefits at age 62.

Family members that qualify for benefits based on your Social Security record

Social Security benefits for children

Your children including biological children, adopted children, step children or dependent grandchildren may qualify for benefits based on your Social Security record. In order to qualify for the benefit, the child must be under the age of 18 and unmarried. If the child is 18-19 years old, the child must be a full time student, but not higher than grade 12. If the child is older than 18, they can also qualify if they are disabled.

Your spouse, ex-spouse or child may receive a monthly payment of up to 50% of your full retirement benefit amount if they qualify for benefits on your record, they . These payments will not decrease your retirement benefit.

Generally, the total amount you and your family can receive is about 150% – 180% of your full retirement benefit.

Eligibility for Social Security survivor benefits

If you qualify to receive the Social Security benefits as a survivor, you can start to receive the benefits from the age of 60 until full retirement age. Note that if you choose to receive your benefit before full retirement age as a survivor, the amount of your benefits will be reduced by some percentage depending on your year of birth.

In addition, if you receive window(er) benefits, but you also qualify for a larger amount of retirement benefits based on your own Social Security record, you will receive a larger amount of benefits. You must be at least 62 to receive your own Social Security benefits. You can talk to a Social Security representative to get help in understanding your retirement benefit options.

If you were born before January 2, 1954, you can choose to delay your benefits if you qualify for benefits as a widow(er), or surviving divorced spouse on another record. Your benefits will be greater if you choose to delay your retirement benefits until you reach your full retirement age or later.

Social Security benefits for divorced spouse

If your ex spouse qualifies for Social Security benefit or disability benefit, you can receive Social Security benefit for a divorced spouse on your ex spouse’s Social Security records. In order to qualify for the benefit, you must be at least 62 years old, divorced from your ex spouse and unmarried. In addition, you must have been married to your ex spouse for 10 years or more. If you remarried, you still can receive the benefit on your ex spouse record if annulment, divorce or death happened to your later marriage.

You can apply for the benefit even though your former spouse has not retired yet if you were divorced for at least 2 years from your ex spouse.

Let’s say your retirement benefits on your own Social Security benefit is larger than the benefits that you receive on your former spouse’s Social Security record or vice versa. Then, you will receive the larger amount of the benefit on either your retirement benefit record or on your former spouse’s record.

When can you apply for Social Security benefits?

When you decide to apply for Social Security benefits, you can apply 4 months prior to when you want your Social Security benefits to begin.

For instance, you want your Social Security benefit to start when you are at the age of 65, then you can apply at the age of 64 and 9 months. Note that you can also apply for Medicare when you will reach 65 within 3 months. With that saying, you can apply for both Social Security benefits and Medicare if you will reach 65 within 3 months.

How to apply for Social Security benefits

After carefully considering the multiple factors listed above, you should decide on your best time to start your Social Security benefits. You can apply for your Social Security benefits by several ways such as by online application, by phone using the provided number 1-800-772-1213 (TTY 1-800-325-0778) or you can apply in person at your closest Social Security office. If you are living in foreign countries and want to apply for your Social Security benefit, you can reach out to the Federal Benefits Unit of the country where you live.

You need to prepare multiple documents applicable to your situation as part of your Social Security application. Note that you can also apply for the benefits of a spouse, family member, or survivor. The Social Security Administration will need all necessary records such as your birth certificate or other proof of age, marriage records, proof of U.S citizenship if you were not born in the U.S, tax documents, U.S military records, bank information and so on. Check out the checklist and get all necessary documents for yourself as well as your spouse and family members.

Questions and Answers – Social Security benefits

1. At what age can you collect Social Security?

You can start to collect Social Security benefits at the age of 62. However, your social security benefits will be reduced by some percentage if you choose to receive the benefits before you reach your full retirement age. If you choose to delay taking the benefits up to the age of 70, the amount of your benefit will increase by up to 8% depending on your year of birth.

2. What is your full retirement age?

The full retirement age has gradually increased beginning with the year of birth 1938 and later. The retirement age goes up a few months for every birth year until it reaches 67 for people born 1960 and later. Check your full retirement age and its impact on the benefit you receive from the full retirement age chart above.

3. How early you can apply for your Social Security benefits

When you decide to apply for Social Security benefits, you can apply 4 month earlier before you want your Social Security benefits to begin.

Note that you can also apply for Medicare within 3 months of 65. With that saying, you can apply for both Social Security benefits and Medicare if you will reach 65 within 3 months.

4. How is Social Security calculated?

Your Social Security benefits will vary based on your age; when you choose to receive the benefits; cost of living adjustment; applicable U.S laws and policies and so on.

You will know the actual amount of your benefit when you apply for it. However you can always estimate your benefits by using the Social Security Quick Calculator, the Retirement Estimator, or the Estimate Retirements Benefits calculator to plan for your future benefit at different ages.

5. May your family members receive benefits based on your Social Security records?

Your spouse, ex-spouse or child may receive a monthly payment of up to 50% of your full retirement benefit amount if they qualify for benefits on your record. Your retirement benefits will not be affected by these payments.

Sources:

Social Security Administration. Retirement. Accessed 7/13/2021